Amid AI Excitement, Landing Customers Proves Tricky...Google's Gemini Gains Ground...Sequoia in the VC Directory

Plus, new deals from Auradine, Collaborative Robotics, Cyera, FloQast, and TORL BioTherapeutics

Hey it’s Madeline.

Quick teaser for you—if you’re a fan of our Cerebral Valley AI Summits, look out for a big announcement from us on Monday. We’re excited to share what’s coming up for us in 2024.

Okay, let’s get into it.

The Main Item

Hot Generative AI Startups Search For Customers

It’s no surprise that first-quarter data shows VC investment in AI startups down from its peak a year ago, when a handful of LLM companies led by OpenAI were raising later-stage rounds in the billions. With overall VC investment in Q1 at its lowest level since 2018, according to Crunchbase, AI didn’t totally buck the trend.

Yet the seed-stage pipeline looks more robust than ever: the latest YC batch was over 50% AI-first companies, according to president and CEO Garry Tan. And there are still plenty of deals being done at all stages: we learned just today that Contextual AI, which fine-tunes LLMs for enterprise customers, is in the process of landing fresh funding, according to three people with knowledge of the deal, one of whom said that existing investor Greycroft is participating.

But we may be entering a new phase of generative AI investing as large LLM companies with nosebleed valuations face the realities of generating revenue and competing with the tech giants, even as a new wave of companies search for the “killer app.”

The big foundation model startups still have runway. AI research lab Cohere, which has announced new LLMs for enterprises—such as CommandR+, optimized for research augmented generation (aka “RAG”)—is in talks to raise $500 million at a $5 billion valuation. Perplexity, the AI-powered search engine, also just raised a new round valuing it at $1 billion, despite admitting that it still relies on some ranking signals from Google to generate its results.

But Cohere had annualized revenue of only $30 million in Q1, a source familiar with the figures said. Perplexity, which charges $20 a month for its consumer-facing search service, had just $20 million in 2023 revenue.

Anthropic, which raised over $7.3 billion in funding last year, expects to post revenue well into the nine figures this year. Its gross margins, which came in at 50% and 55% in December of last year, according to The Information, are much lower than for similarly-sized public software companies, pointing to the complicated road ahead.

Inflection AI, another high-priced startup, had scaled back ambitions on its much-touted Pi chatbot even before co-founder Mustafa Suleyman and key members of the team defected to Microsoft.

Two investors told me on background that they expect a lot of AI startups to fall from grace in coming months as they fail to win customers quickly enough. “I think you're going to have this revenue traction not come to fruition for a lot of them that are really good tech but not necessarily things people want to pay for,” said one of the investors.

The industry as a whole seems to be entering what’s historically been one of the toughest phases of innovation: when the technology has shown itself to be spectacular, but it’s still not entirely clear exactly what it’s good for, and what people will pay for. Think of the Apple Macintosh circa 1985, or the Palm Pilot, or VR.

On the consumer side, the generative AI “killer app” has yet to appear: accurate voice-recognition and language translation might be the closest thing. There are plenty of obvious uses in the enterprise, but it’s still not obvious how people will use generative AI day-to-day, even though the novelty value is very high.

For AI firms aiming to sell to businesses, accuracy and compliance are the big issues slowing adoption, investors say. Costs are a factor too: even Microsoft’s corporate customers aren’t sure a chatbot is worth the money.

“The AI tulipmania of 2023 is giving way to reality given slower adoption in the enterprise,” said Mayfield’s Navin Chaddha. He said he’s still excited about AI startups “at the plumbing layer” of the AI stack, such as middleware, infrastructure software, and the semiconductors adjacent to GPUs.

AI-presentation maker Tome shows the predicament for consumer apps. Executives there are reportedly debating whether to shift to prioritizing business customers, after consumers proved perfectly content to use a free tier without ever converting to paying subscribers, The Information reported. The company has raised $81 million to date from investors including Greylock and Coatue.

Tome’s situation points to another challenge for AI startups: the strength of ChatGPT and the incumbent tech giants. Enterprise customers might be more willing than consumers to pay for an AI-powered PowerPoint tool—but they might also be more likely to buy it from Microsoft.

OpenAI’s annual revenue rate is already at $2 billion and growing, in part due to its enterprise contracts. And after weeks of critical press, Google unveiled a slew of new updates to Gemini for enterprise customers on Tuesday, including the ability to boost accuracy and transparency by integrating Gemini’s answers with Google search results.

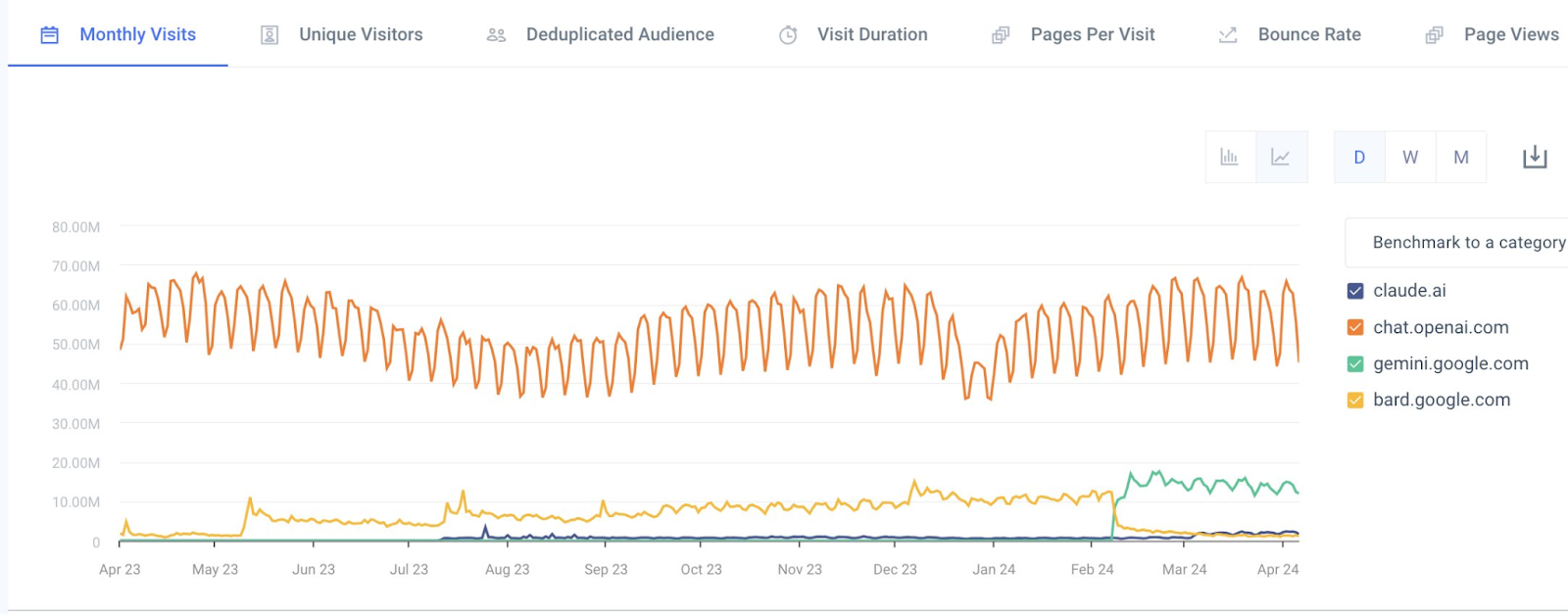

Gemini’s traffic is already at 25% of ChatGPT’s, and that’s without fully integrating it into its hugely-popular GSuite and Android interfaces. Google seems ready for aggressive moves that will put even more pressure on AI startups counting on paying corporate customers.

One Big Chart

Chatbot Traffic Month over Month

Some AI investors say any skepticism is overblown. One told me on background that the “AI sales cycles” for larger enterprises have simply not been established yet, but once the AI is fully integrated with complex data and compliance procedures, customers will begin to see real results.