Venture Funds' Markups Stagnate & Distributions Underwhelm As Startups Remain in a Contraction Period, Per AngelList's New Annual Report

'The good news, if there is any, is 2024 stopped getting worse.'

Venture funds from every recent vintage managed on AngelList have seen their total value stagnate since the massive valuation run-up into 2021.

That’s one finding from AngelList’s annual report on the state of startups and venture capital, based on the activity that it sees on its fundraising platform.

Overall the report paints a bleak picture of U.S. startup activity in 2024.

Even as artificial intelligence deals skyrocketed, many startups raised down rounds or avoided fundraising at all.

“The story of 2023 was every month got worse than the last month — it started pretty bad and got really bad,” said Abe Othman, a researcher at AngelList. “The good news, if there is any, is 2024 stopped getting worse.”

AngelList says that “the venture capital ecosystem’s health has been historically low for the past two years.”

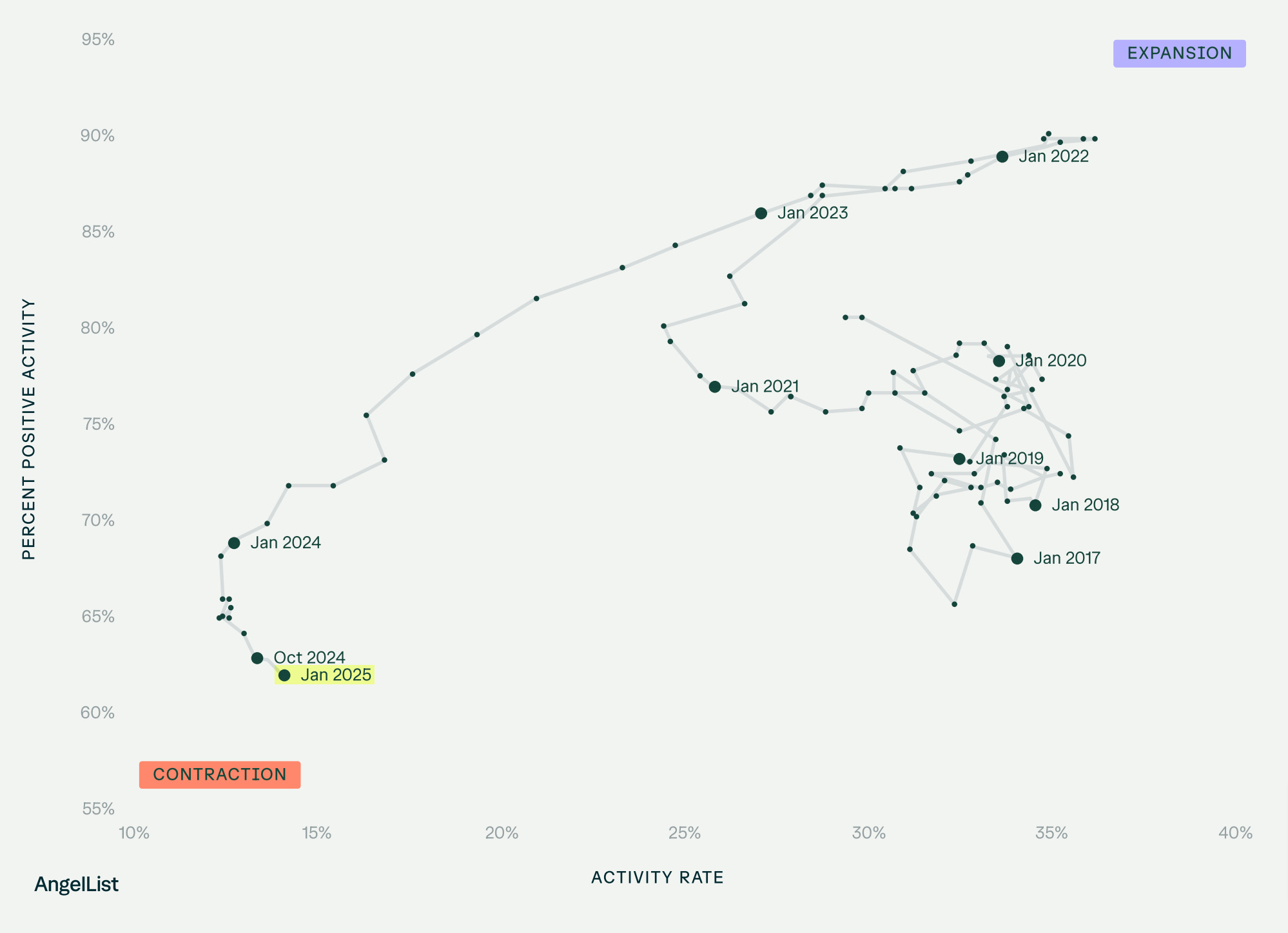

AngelList tracks positive activity (up rounds and exits that return money to shareholders) and then activity (how many startups on its platforms are raising money or exiting). Put together, the two measures give a feel for how well things are going in the startup industry. We started 2025 in the worst quadrant — “contraction.”

AngelList reports:

Of the 16,000+ active US startups with seasoned investments on the platform before 2024, only 14.2% experienced a price-per-share change in 2024. When looking into those changes even further, just under 62% of those changes were positive. This makes the annual activity rate close to its historic low (lowest being set earlier in 2024), while the tenor is at a historic low. Put another way, not many startups changed their price per share over the past year, and the changes we did see were more negative than at any time in our data set.

This is the second time that AngelList has first shared its annual report on “The State of U.S. Early-stage Venture & Startups” with Newcomer readers. “Given the visibility and really the timeliness of our data we can be a little stronger in our conclusions than other sources,” Othman said about the report.

AngelList is able to observe startup performance by tracking startups on its platform and the startups that receive investments from venture firms on AngelList. Meanwhile, AngelList has visibility into the performance of venture funds managed via AngelList, as well as many smaller, emerging managers. Funds hosted on AngelList’s platform have raised more than $4 billion over the last three years.

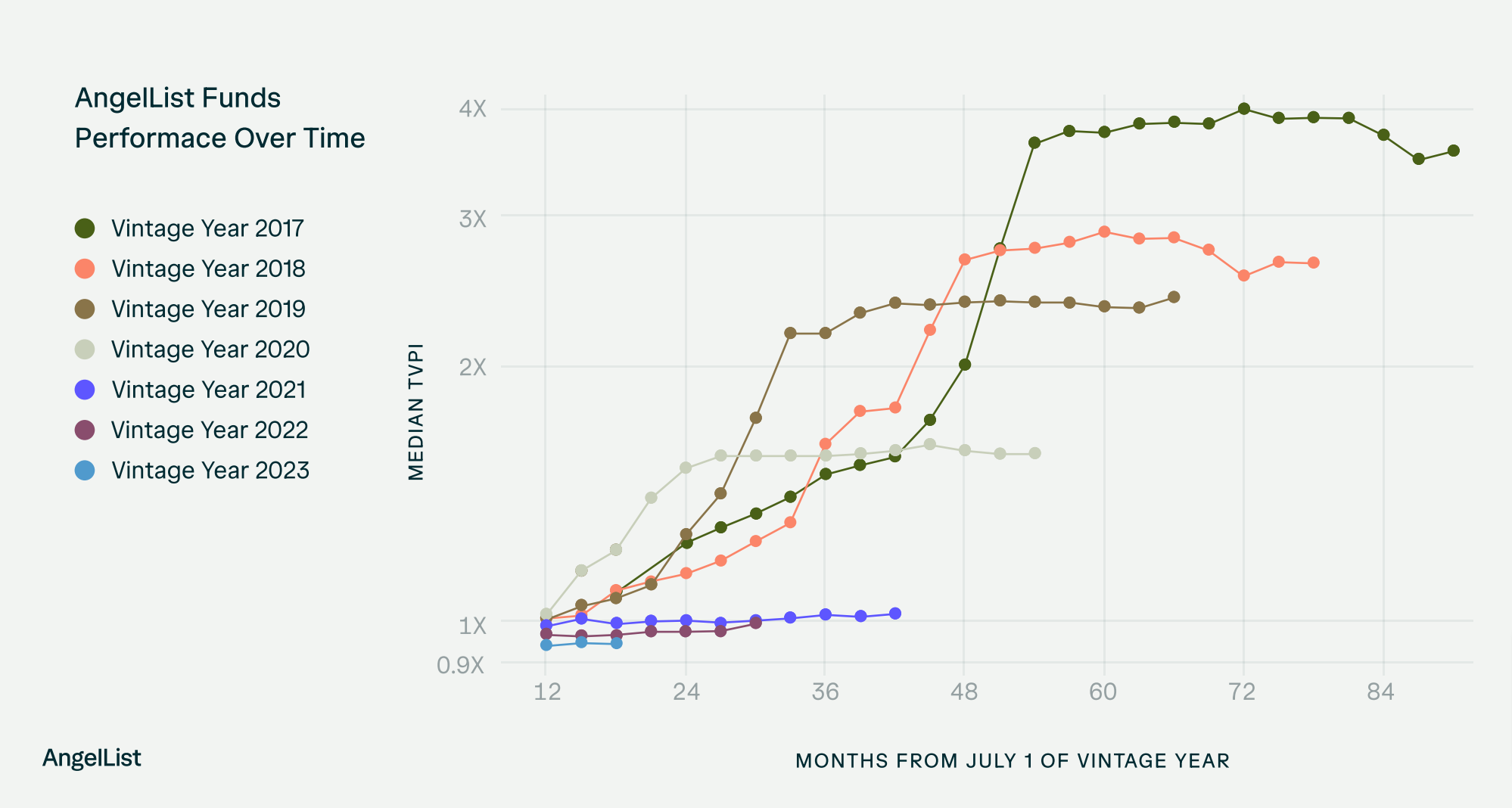

For the first time this year, AngelList is disclosing the aggregate performance of venture capital funds managed on its investing platform.

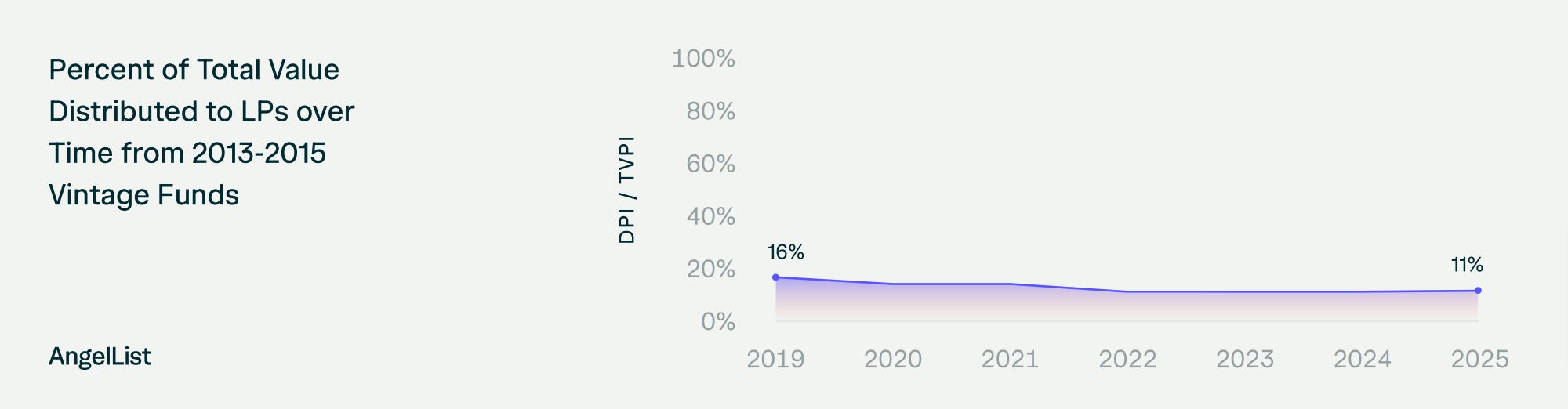

While some of the earlier vintages have seen meaningful markups, accumulated during the bull run, there haven’t been meaningful distributions so far.

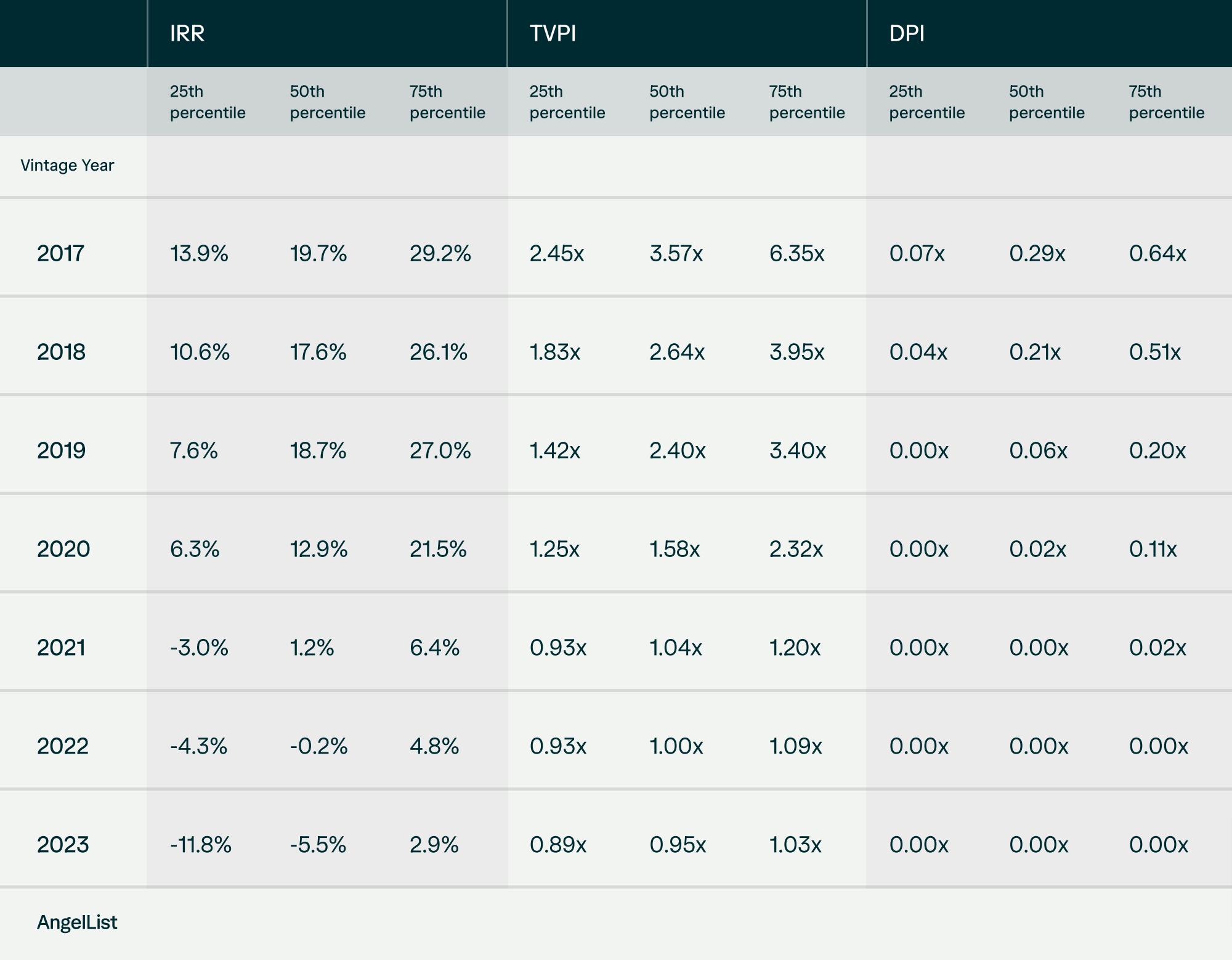

Eight years out, the median 2017 vintage fund has 0.29x distributed to paid-in capital (DPI), compared to 3.57x total value to paid-in capital (TVPI). That means funds are sitting on hefty paper markups without seeing enough exits to return even half of what limited partners initially put into venture funds. (AngelList’s fund data reflects venture funds managed on its platform, meaning they skew toward smaller, emerging fund managers. The median fund on the platform during the period covered by the table above had about $4 million to invest.)

These VC funds will need to find a path to exits — waiting for startups to find buyers or go public, or selling their positions to other private investors. Otherwise, funds will be forced to start cutting their view of the value of their startup investments.

This year will be a crucible moment for venture firms, revealing whether valuations will hold or if reality will force a reckoning.

The chart above is a complex but important one.